There are five Ps of Sustainability Development Goals

People | Planet | Prosperity | Peace | Partnership

Triple Bottom Line - People, Planet and Profit

Development

Goals

There is a general misunderstanding that CSR is the same as Corporate Philanthropy, and hence giving away for charity is often misconstrued as the only CSR activity a corporate organisation needs to engage in.

Although philanthropy may be a part of the CSR strategies of a business, there is much more to CSR than simply philanthropic gestures, and charitable initiatives.There are five Ps of Sustainability Development Goals

People | Planet | Prosperity | Peace | Partnership

Triple Bottom Line - People, Planet and Profit

There is a general misunderstanding that CSR is the same as Corporate Philanthropy, and hence giving away for charity is often misconstrued as the only CSR activity a corporate organisation needs to engage in.

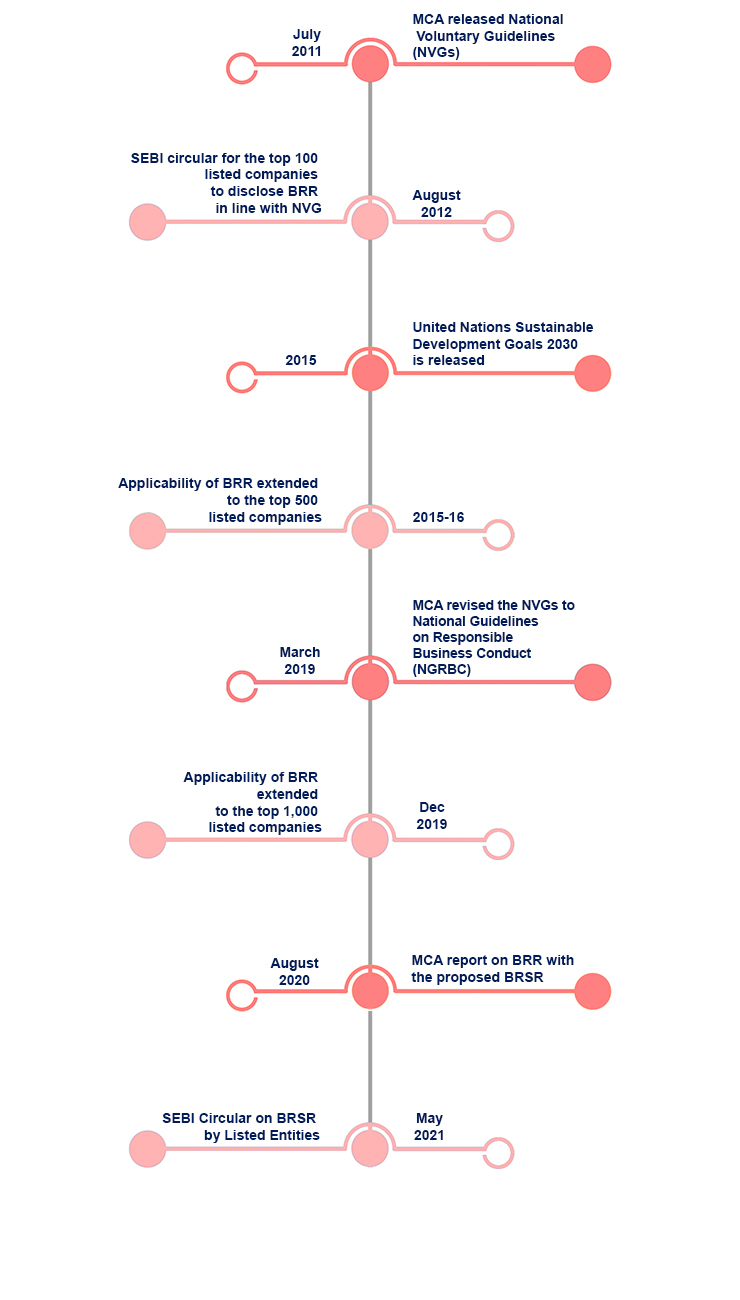

Although philanthropy may be a part of the CSR strategies of a business, there is much more to CSR than simply philanthropic gestures, and charitable initiatives.Timeline of ESG Evolution

Jargons Simplified

ESG Jargons Simplified

BRSR Reporting Structure

COVID further accelerated the relevance of Environment, Social and Governance (ESG) considerations amongst investors and other stakeholders resulting in increased awareness and activism on their part.

Reporting of entities performance and disclosure requirements for non-financial information needs to keep pace with this change and the mandate of BRSR is a significant step towards this direction. As per the amendment to Regulation 34 (2) (f) of LODR Regulations vide Gazette notification no. SEBI/LAD – NRO/GN/2021/22 dated May 05, 2021, SEBI has introduced new reporting requirements on ESG parameters called the Business Responsibility and Sustainability Report (BRSR).

The format for BRSR is accompanied by a guidance note to enable the entities to interpret the scope of disclosures.

As per the new reporting requirements, with effect from the financial year 2022-2023, filing of Business Responsibility and Sustainability Reporting (BRSR) shall be mandatory for the top 1000 listed companies (by market capitalization) and shall replace the existing BRR. Filing of BRSR is voluntary for the Financial Year 2021-22.

Section A

General Disclosures

Basic information about the company (size, location, products, number of employees, CSR activities, etc.)

Section B

Management and Process Disclosures

Policies and processes relating to the principles laid out under NGRBC around leadership, governance and stakeholder engagement

Section C

Principle-wise Performance Disclosures

(Actions and Outcomes) How company is performing on each of the principles and core elements

- Essential (Mandatory)

- Leadership (Voluntary - Opportunity to show greater impact and outcomes)

BRSR Reporting or BRSR Lite Reporting can be voluntary adopted by other listed and unlisted companies.

As well, it is foreseen that BRSR Reporting will sooner or later become applicable to all listed and unlisted entities (including private limited entities)

Key Offerings on ESG

Sustainability Adoption and Implementation Services

We can enable policy mapping and drafting in the correlation of the existing framework to adopt sustainable measures. We can undertake the implementation of a sustainable approach - function/department specific and otherwise generic for industry-agnostic measures.

This would include policy drafting, aligning and mapping current policies with sustainability and its reporting requirement, enabling the implementation of the policies – framing procedures around the same and monitoring of the same.

Reporting and Compliance Support Services

We can take the role of an extended team of the organisations to equip and prepare for the Reporting and assist in managing the compliance documentation. We shall as well implement a digital workflow approach to reduce the time efforts required towards reporting and compliance activity.

This would include BRSR Reporting, GRI Reporting, SDG Reporting and IIRC Reporting along with developing internal tools and digital workflows to enable seamless compliance and collation of data from multiple sources.

Strategic Consulting on Driving Sustainability

We can work closely with the leadership team in the management to align the interest of the Board in terms of taking strategic decision making to create a proactive measure towards sustainability. We can recommend key drivers about sustainability specific to the entity to drive the culture and walk the talk in the industry towards taking aggressive measures, which can enable a positive impression and footprint.

This would include developing KPIs that support strategic and sustainable goals, providing strategic recommendations, Applying management accounting tools and techniques, such as scenario planning of natural resource availability, lifecycle costing, and helping integrate sustainability matters into the decision-making process.

Diligence and Assurance Support in CSR and Sustainability

We can perform diligence checks on the CSR spending as well as support organisations to get vetted on their credentials and activities. We can facilitate diligence checks for financial institutions, credit rating agencies and investors from a sustainability standpoint.

This would include performing diligence during raising funds, monitoring the funds deployed, produce reports which include data on business impacts on sustainability. It would inform stakeholders about strategic planning and various decisions are taken like budgeting and pricing decisions, investment appraisals.

Key Offerings on ESG

We can enable policy mapping and drafting in the correlation of the existing framework to adopt sustainable measures. We can undertake the implementation of a sustainable approach – function/department specific and otherwise generic for industry-agnostic measures.

This would include policy drafting, aligning and mapping current policies with sustainability and its reporting requirement, enabling the implementation of the policies – framing procedures around the same and monitoring of the same.

We can take the role of an extended team of the organisations to equip and prepare for the Reporting and assist in managing the compliance documentation. We shall as well implement a digital workflow approach to reduce the time efforts required towards reporting and compliance activity.

This would include BRSR Reporting, GRI Reporting, SDG Reporting and IIRC Reporting along with developing internal tools and digital workflows to enable seamless compliance and collation of data from multiple sources.

We can work closely with the leadership team in the management to align the interest of the Board in terms of taking strategic decision making to create a proactive measure towards sustainability. We can recommend key drivers about sustainability specific to the entity to drive the culture and walk the talk in the industry towards taking aggressive measures, which can enable a positive impression and footprint.

This would include developing KPIs that support strategic and sustainable goals, providing strategic recommendations, Applying management accounting tools and techniques, such as scenario planning of natural resource availability, lifecycle costing, and helping integrate sustainability matters into the decision-making process.

We can perform diligence checks on the CSR spending as well as support organisations to get vetted on their credentials and activities. We can facilitate diligence checks for financial institutions, credit rating agencies and investors from a sustainability standpoint.

This would include performing diligence during raising funds, monitoring the funds deployed, produce reports which include data on business impacts on sustainability. It would inform stakeholders about strategic planning and various decisions are taken like budgeting and pricing decisions, investment appraisals.